Changes are Coming to the AHCA

Speaker Paul Ryan is changing his tune, declaring that modifications are needed to make it possible for the American Health Care Act (AHCA) to pass the House. This is a clear departure from his comments last week which suggested the AHCA was a “binary choice” and that this version was the “closest we will ever get to repealing and replacing Obamacare.”

On Wednesday, while giving a brief civics lesson on how a bill becomes a law, Ryan explained that through the four-committee process in the House “we make refinements and improvements to the bill.” Then, when it goes to the Senate, “if they want to make changes or improvements to the bill, they’ll have that opportunity because that’s how bills become law.” Or, to put it in President Trump’s words, the health care bill will be the product of a “big fat beautiful negotiation.”

Ryan also asserted that these modifications will come in the context of the Congressional Budget Office (CBO) report: “Now that we have our score from the CBO, that’s something we were waiting for … we’ve got room to make refinements.” The construction of premium tax credits in the AHCA may be one provision that is up for debate as this bill moves ahead. To better understand the implications of premium tax credits on coverage and affordability, let’s explore:

- How the Affordable Care Act (ACA) and the AHCA structure premium tax credits differently; and

- Why the CBO findings of lower average premiums and market stability depend on the design of premium tax credits.

Differences in Premium Tax Credits Contribute to CBO Coverage Estimates

Starting in 2020, the AHCA would provide refundable tax credits that increase based on age (ranging from $2,000 and $4,000), but phase out for individuals with incomes above $75,000.

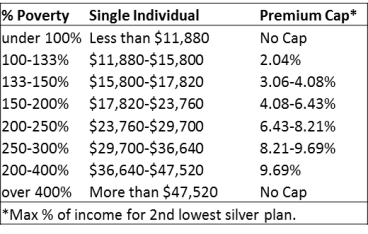

In contrast, the ACA tax credits actually operate as a premium cap. Under the ACA, premium tax credits are provided on a sliding scale for individuals between 100 and 400 percent of the Federal Poverty Level (FPL), or in dollars, individuals with incomes between $11,880 and $47,520 per year. This means that people in this income range have caps on the premiums that they pay, based on a percentage of their income (see Table 1).

Table 1. 2017 Premium Caps Based on Income in ACA

In other words, the federal government pays a premium subsidy that is equal to the difference between the percentage of income individuals are required to contribute and the cost of the 2nd lowest cost silver plan (i.e., the benchmark plan). For example, individuals up to 200 percent FPL will pay no more than 6.43 percent of their income in premiums, or a little more than $1,500 per year, and the federal government would pick up the rest, up to the cost of the 2nd lowest cost silver plan.

What Does this Mean in Practice?

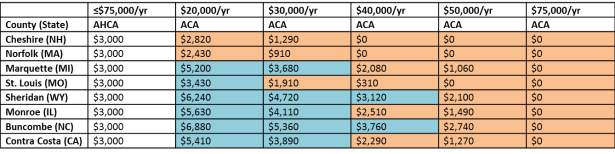

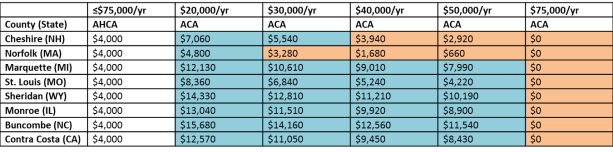

Remember that Kaiser interactive map, illustrating how people of different incomes and ages would fare in the ACA vs. the AHCA in 2020? Specifically, it shows the size of the premium tax credit for a person of a specific age, income, and county. Because the ACA premium tax credits operate as caps, and the costs of the benchmark plans vary based on age and where you live, the ACA credits will enable older adults and people in higher cost areas to get higher subsidies.

To bring this to light in a different way, the tables below show a handful of counties. For each county, the size of the tax credit under the AHCA and the ACA is compared for both a 40 year old and a 60 year old across different incomes. As in the Kaiser map, blue cells show where individuals would receive higher tax credits through the ACA, whereas orange cells show where individuals would receive higher tax credits through the AHCA.

Table 2. Amount of Premium Tax Credit for Forty Year Old, By Income

Table 3. Amount of Premium Tax Credit for Sixty Year Old, By Income

It is clear that the ACA premium tax credits, relative to the AHCA, are more beneficial for those who are older, poorer, and live in high cost areas. Even more, because these tax credits account for varying costs related to age and where you live, and are capped based on a percentage of income, they are able to protect lower income people from increases in health insurance premiums for purchases made through the exchanges.

So, how do premium tax credits play a role in two critical findings from the CBO report?

By 2026, average premiums for individuals in the nongroup market would be 10 percent lower relative to current law.

Average premiums may ultimately go down under the AHCA but that is not cause for celebration. Rather, the CBO suggests that average premiums for people purchasing health insurance in the nongroup market (i.e., people who purchase health insurance coverage independently, not through employers) would increase 15 to 20 percent between 2018 and 2019 when the individual mandate is eliminated, because fewer healthier people would sign up.

By 2026, relative to the ACA, premiums would be significantly lower for younger adults, and significantly higher for older adults:

- Premiums for a 21 year old would be 20 to 25 percent lower

- Premiums for a 40 year old would be 10 percent lower, and

- Premiums for a 64 year old would be 20 to 25 percent higher.

Then, because the AHCA premium tax credits will not adequately protect poorer, older adults from the burden of high and rising premiums, eventually the risk pool would change. So, as younger, healthier people are able to sign up with lower premiums, older sicker people will be priced out of the market, and ultimately become uninsured. So, yes, average premiums for those who are insured will go down, but those who need health insurance the most will be put out to pasture.

You see here Speaker Paul Ryan’s misunderstanding of the very purpose of health insurance. In other words, the design of the AHCA rejects the premise that the point of health insurance is in fact to have the healthy, younger people subsidize the sicker, older people. Instead, the cost problem of high premiums is addressed by moving around the deck chairs and changing who is in and who is out—not by fundamentally tackling the problem of rising health insurance premiums for everyone.

The nongroup marketplaces would be stable either way.

Despite the rhetoric driving the ACA replacement debate, namely that Obamacare is collapsing into a death spiral, the CBO estimates that under both current law and the AHCA, the nongroup markets would be stable.

The CBO suggests that the main reason that the insurance markets under the ACA would be stable is the combination of (1) the presence of the individual mandate—incentivizing healthy people to come into the market—and (2) that low-income populations are protected from premium increases in the nongroup market.

It is true that premiums in the nongroup market increased significantly this year. However, experts suggest that while there was a bit of a market correction in the past year, the marketplaces should be stable going forward. Moreover, through the ACA, upwards of 80 percent of people who buy insurance through the health insurance exchanges get premium tax credits (i.e., premium caps), and would therefore, not bear the cost of rising premiums. Instead, estimates suggest that only three percent of Americans feel the impact of rising premiums in the health insurance exchanges. This group either has incomes that are too high to be eligible for premium tax credits, or choose to purchase a more expensive plan beyond what the subsidy will cover. The relatively small group impacted by premium increases in the health insurance exchanges is a critical point that gets lost in the debate over rising premiums and Obamacare.

An Aside for Health Policy Wonks: Now, critics of this 80 to 85 percent figure often cite that there is a group beyond this remaining 15 to 20 percent, about 5 to 7 million, who purchase nongroup insurance outside of the exchanges. Importantly, ACA premium tax credits are only available to people who purchase insurance through the exchanges, so this group would not be eligible for government subsidies. This group is harder to characterize due to lack of reliable data, but experts suggest that this group may be higher income, or at least above the income eligibility level for premium subsidies, and choose to purchase off-exchange coverage to have more choices and less restrictive provider networks. Importantly, data on rising premiums are within the health insurance exchanges, and thus off-exchange nongroup insurance purchases require an entirely separate analysis. Still, it is worth noting that this other cohort, who is also in the nongroup market, exists. Notably, the AHCA would permit premium tax credits to be used for off-exchange purchases of health insurance.

In contrast, because of the way premium tax credits are structured in the AHCA, namely a flat amount of money to use toward the purchase of insurance (as opposed to a cap on how much people are required to spend), more people—particularly more older, poorer people—would feel the impacts of rising premiums in the nongroup market.

Now, given the differences in how premium tax credits are constructed, why is the CBO saying the markets would also be stable in the AHCA? This is interesting as well. They argue that market stability would result from the combination of eliminating requirements that plans meet certain actuarial values (i.e., less robust health insurance coverage) and a younger mix of enrollees who are likely to sign up due to lower premiums. This explanation relates to the first point about lower average premiums. In other words, the market is likely to be stable because the sicker, older people are less likely to be part of it, since they will have been priced out of the market. This leaves the remaining insured population relatively younger and healthier—exactly the type of risk pool that insurance companies want to cover.

The CBO also suggests that the AHCA’s newly created Patient and State Stability Fund would stabilize the nongroup market. While the Patient and State Stability Fund could be used in a number of ways, the CBO estimates that states will predominantly use it to limit insurers’ costs due to very high claims of enrollees, which would encourage insurers to continue to offer coverage in the nongroup market. Again, this would provide further protection for insurance companies when they cover those relatively healthier people who happen to have a really high claim or get a really expensive diagnosis during the year. In other words, it protects insurance companies from taking on too much risk, and therefore, stabilizes the markets.

What are the Implications?

The differences in the construction of premium tax credits highlight three important points:

- The less robust government subsidies in the AHCA for older, sicker people make it more likely that they will be priced out of the market, thus bringing down average premiums among the relatively healthier insured population.

- Under current law, given that the government is taking on the burden of the majority of premium increases, the ACA nongroup market is not unstable as the Republicans would have you believe. Rather, higher premiums for those eligible for premium tax credits are picked up by the federal government.

- Clearly, the premium tax credits in the ACA cost more money (and in turn are of more value) relative to those offered in the AHCA. Thus, their elimination (and replacement with less robust age-based credits) contributes to some cost savings noted in the CBO report.

By all accounts, the CBO report is a bad sign for the AHCA. Keep an eye on any changes to the design of the premium tax credits as the bill moves through the House and Senate.

Wow, where to begin. Signe, I am so glad you understand all this.

Sent from my iPad

>

LikeLike